It's a marathon, not a sprint

Summary:

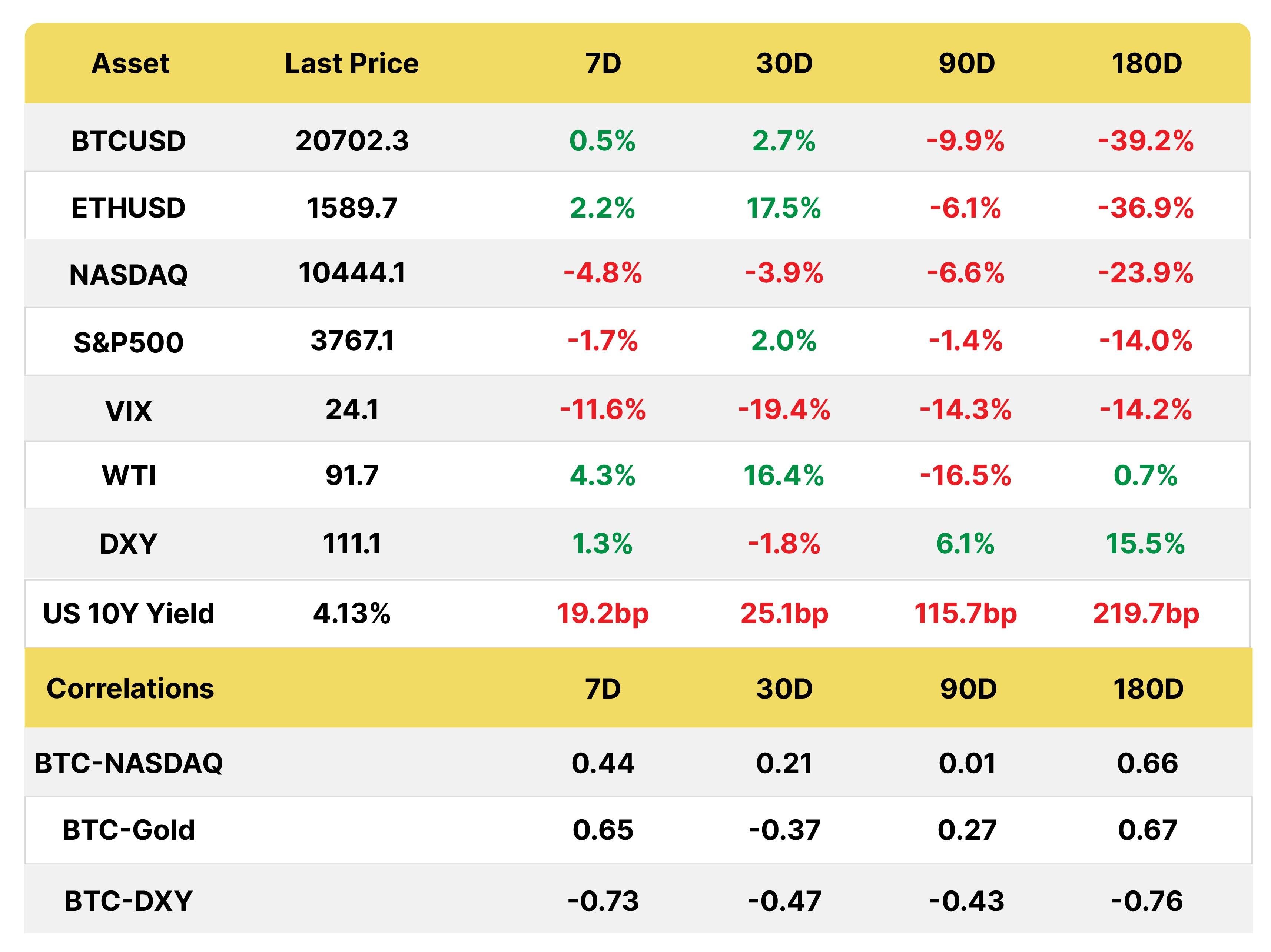

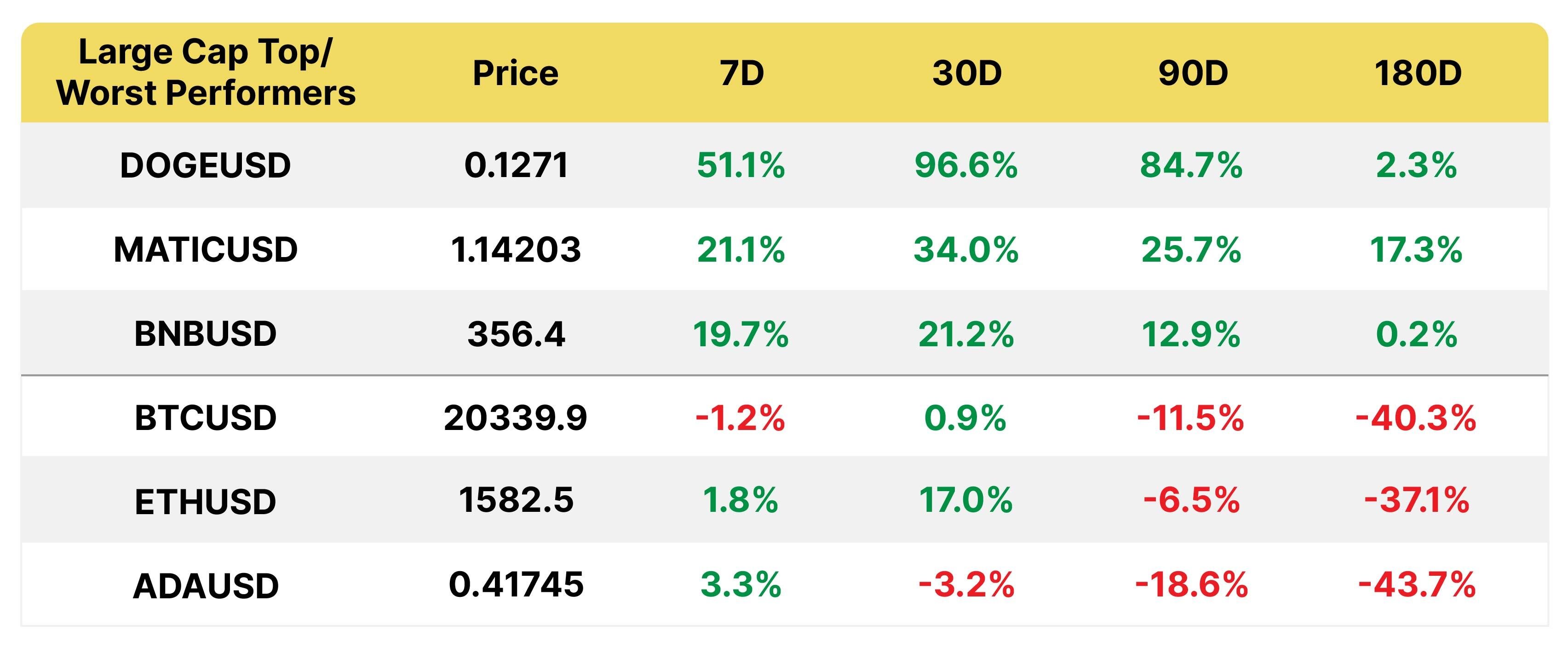

The ongoing monetary cycle will be longer than you think though probably less steep, according to the Fed. This was a more bearish tone than expected and increasing recessionary signals don’t bode well for discretionary stocks that saw abnormal returns during Covid. The NFP and unemployment data on Friday did nothing to change that. In crypto, BTC price action is like watching paint dry, with outperformance around Twitter-related names BNB, MASK, DOGE and also MATIC due to the Insta NFT integration. A more substantive event was the tokenized cross-currency swap on Polygon under a Singapore scheme that included JP Morgan. Tokenizing financial assets could generate tens of billions of dollars in savings, according to a recent report. That’s without considering what could be done in trade finance and wealth management.

Macro

RATE HIKES: THE TALONS ARE OUT

Just as this time last year we were recording new highs in equities, this was a week of multi-year highs in the two-year yields. Rates raced past the 4.60% posted just two weeks ago, to over 4.70%, on their way to 5%, pricing in a more hawkish monetary policy in the short term post-FOMC. This steepened the 10/2 curve even more to -59 bps on fears the Fed will overdo it and their comments that the path to a soft landing has narrowed. The bond market clearly thinks the path has been entirely obstructed so at some point, but not yet, they will have to pivot.

The 75 bps hike came as no surprise (+3.75%YTD) and the accompanying statement was read as dovish, causing a short-lived move up in stocks and dollar weakness, as the Fed said it would consider the cumulative tightening so far and its lagging effects. But the real action was Chairman Powell’s comments which proved more hawkish than even the bears imagined, as opposed to the BOE’s dovish message as officials here forecast a two-year recession.

The result was a swift repricing of the yield curve on the remarks, notably that the risk is that they don’t hike enough and that the terminal rate is higher than their previous estimates (4.96%)! He acknowledged the slowing economy, including housing and consumer spending and slower business fixed investment, but also the tight labor, high wages and particularly the latest CPI report.

So even though the pace of hikes may slow, perhaps as soon as December, to +50 bps which is what the market is pricing, the endpoint may be higher. This means at least another 150 bps to go. Powell also emphasized that it was premature to discuss pausing, which threw cold water on the bulls.

|

“...if we over tighten, and we don't want to, we want to get this exactly right, but if we over tighten, then we have the ability with our tools, which are powerful, as we showed at the beginning of the pandemic episode, we can support economic activity strongly if that happens. On the other hand, if you make the mistake in the other direction, and you let this drag on, then it's a year or two down the road and you're realizing inflation behaving the way it can, you're realizing you didn't actually get it, you have to go back in.” Jerome Powell |

Perspective: Another 20 bps yield curve inversion since Powell spoke, lows not seen this century

Source: Bloomberg

Growth in consumer spending has slowed from last year, in part reflecting lower real disposable income and tighter financial conditions but is proving resilient

The JOLTS September jobs report was stronger than expected (10.72 mn job openings) with the Fed citing a tight labor market, high wages and vacancies as reasons to keep going on rates

THE BIS ON KING DOLLAR: NO PIVOT BUT WARNS OF TRIPWIRES

Proving timely given the Fed action this week, the Bank for International Settlements (BIS) published a report on global exchange adjustments, notably the strengthening of the dollar against most currencies to its highest level in 40 years. The BIS acts as the banks’ bank, with its mission to support central banks’ pursuit of monetary and financial stability, so the strong currency moves are clearly an area of concern for them.

Established in 1930 to facilitate war reparations, it is owned by over 60 central banks, promotes cooperation and provides banking services for these institutions. It was almost abolished post-WW2 but regained importance with the end of the gold standard when more international cooperation was needed in the face of instability.

The report focuses on the role that the USD plays as an invoicing currency, meaning it raises import prices for other countries. Unusually, dollar strength has happened at the same time commodity prices surged, generating an inflationary double-whammy. It has also meant tighter financial conditions.

1 Monthly average of Federal Reserve Board trade-weighted real US dollar index, based on trade in goods and services.

Source: BIS

The BIS admonishes that countries must have a consistent macro stance to ensure financial stability (we’re talking to you, UK). Fiscal and monetary policy needs to be on the same page to avoid disruptive FX moves due to fears of fiscal dominance.

Cause: In addition to interest rate differentials, the US has also enjoyed better terms of trade. The country is now a net energy exporter, in particular gas, a big change from the past. This is breaking the traditional inverse relationship between the greenback and commodities, as is the war in Ukraine via impacts on food prices. Finally, a flight to safety has benefited the dollar.

Effect: The dollar dominates trade invoicing, trade financing, cross-border payments and funding in global capital markets. The USD was on one side of 88% of all FX trades in April 2022, unchanged from the 2019 survey, so there are no signs that dollar dominance is fading. The renminbi only rose marginally from 4% to 7%.

The result is less trade as countries import less and cut dollar financing. It also means higher cost of financing for corporates and sovereigns and less appetite for risk. According to the BIS, it is hard to know what the impact will be from these swings.

This time around, emerging economies are less reliant on FX borrowing and have better macro frameworks than in the 80’s and 90’s, but corporates have much more exposure. Overall, debt levels are much higher. The tripwires won’t be the banks but nonbank financial intermediaries and the capital markets.

Emerging markets (EMEs) are in better shape now but corporates are more exposed and overall debt levels are higher

Source: BIS

Contrary to those hoping for a Fed pivot, the BIS caution against assuming authorities are overreacting to inflation as rates remain negative in most regions. The bank also believes officials have tools to mitigate strategically in the markets if there is stress, including FX intervention.

Crypto

MATIC, the Polygon network token, which we have written about previously, maintains its momentum as Robinhood selects it for its Web3 beta wallet and META for the minting and sale of NFT on Instagram. TVL at $1.62 bn has remained stagnant compared to Arbitrum, driven by GMX, as TVL approaches Polygon levels.

Polygon was founded in 2017 with the aim to solve the high transaction fees and network congestion on Ethereum, without impacting security by processing the transactions itself.

The chain has the potential to process up to 7,200 transactions per second (TPS).

MEME COINS MAKE A COMEBACK

BNB and Doge were up for the week and month due to the narrative around Twitter. DOGE is now number 8 in terms of market capitalization, at over $17bn and is only behind BTC and ETH in volume traded. Though at its peak in May 2021 it got close to $85 bn in market cap as Elon Musk hosted SNL. Open interest skyrocketed from $150mn on October 25 to $1bn on Monday. This is not far off the 2021 OI levels, though the meme coin’s price was 0.70 cents at that time.

After providing $500 mn in financing to Musk for the Twitter acquisition, Binance launched an index including DOGE, BNB, and MASK, the “Bluebird Index.” BNB is the token of the Binance Smart chain while MASK is the native governance token of MaskDao, which allows users to bridge into Web3 within existing Web2 platforms.

The CEO of Tesla may have plans to decentralize the social media platform after the $44bn acquisition and has hinted that DOGE could be used as a means of payment, for the $8 blue tick subscription that he has implemented, for example. However, the coin, which was created as a joke by the developers, is not ready for prime time as it does not have the scalability needed for such a vast undertaking, at 33 TPS, if it is to be onchain. It is also Proof of Work, something which Musk has cited as a reason to withdraw BTC payment options for his products.

DOGE worked its way back up into the top ten on Twittermania but gave back gains as the Fed said we have a ways to go on tightening financial conditions

MASK, propelled into the spotlight as part of the Binance basket, is up +183% with a market cap of $214 mn, with traded volume rising to >$1 bn per day. Total supply is 100mnm, of which 29mn is in circulation. Funding rates turned steeply negative on November 3 and remain in the red, which is not the case for Dogecoin as traders are still slightly positive on the latter. Investors got in during in five rounds at between 0.08 and .50 cents.

Source: Lookonchain, MaskNetwork

DEX VOLUME SHOWS SIGNS OF LIFE

After very low volume for most of the month of October, DEX activity picked up as markets got excited ahead of the Fed November meeting, with another spike on the day of the meeting itself, November 2, Uniswap led the charge with volume up 123% over one month to $2.1bn, with DEX volume totalling $3.4bn.

Source: Nomics

SINGAPORE AND TRADFI’S PERMISSIONED TOKENIZATION EFFORTS

Even as Singapore’s central bank plans to raise the threshold for retail investors to trade crypto, it is proceeding with several interesting tokenization pilots with various banks, including JP Morgan. After branding itself a crypto hub, there have been several high-profile failures of firms based there, including Three Arrows Capital and Hodlnaut.

In a case of shutting the barn door after the horse has bolted, authorities are proposing that customers’ assets be kept separate from the companies’ own to mitigate the risk of loss or misuse of assets, and also plan to restrict exchanges from lending retail investors’ assets. They are also looking at expanding stablecoin regulation.

Nevertheless, they are far from giving up on the technology. This week, the Monetary Authority of Singapore (MAS) announced its first permissioned cross-currency transaction on blockchain, involving DBS Bank, JP Morgan’s Onyx and SBI Digital Asset Holdings on the Polygon blockchain, forking the permissioned Aave Arc and Uniswap protocols.

This is an interesting development as JP Morgan has three private blockchains for data and some dollar transactions, so maybe the future will be public. It was also telling that they chose an Ethereum scaling platform and that KYC was done onchain rather than the way permissioned pools operate today with gatekeepers doing that work.

A live cross-currency transaction involving tokenized JPY and SGD deposits was undertaken, including instantaneous trading, clearing and settlement. There was also a simulated exercise involving the buying and selling of tokenized Singapore and Japanese government bonds. This reduces costs of using intermediaries and managing counterparty relationships.

It is not the first time the Singaporeans and banks have experimented with digital ledger technology. MAS carried out its first cross-currency payment with digital currencies with the Bank of Canada back in 2019 for a symbolic $100. It was the first such operation between central banks, both based on different DLT platforms.

SocGen and the European Investment Bank have issued bonds on blockchains in the past. Expect the banks and exchanges to keep experimenting. According to a recent report by CB Insights, moving securities onto blockchains could save up to $24 bn per year in trade processing costs, as the four largest banks alone hold $12 trillion in assets.

The savings arise because to conduct a trade you need to keep track of who owns what through a complex web of brokers, exchanges, depositaries, clearinghouses, and custodian banks. The system is based on paper ownership that is slow (1-3 days), inaccurate and vulnerable to fraud. It is even worse when considering electronic trades.

Singapore also launched another two pilots:

- Trade Finance: Standard Chartered Bank is leading an initiative to explore the issuance of tokens linked to trade finance assets. The project aims to digitize the trade distribution market, by transforming trade assets into transferable instruments that are more transparent and accessible to investors.

As per CB’s report, the use of blockchain can support cross-border trade transactions that would otherwise be uneconomical because of costs and documentation processes. It would also shorten delivery times and reduce paper use. Up to 90% of world trade relies on trade finance so it is a problem worth tackling. One of the biggest risks is fraud, which could be eliminated if payments can be done in tokenized form contingent on delivery, with smart contracts.

Through blockchain technology, payments between importers and exporters could take place in tokenized form contingent upon delivery or receipt of goods. Through smart contracts, importers and exporters could set up rules that would enable automatic payments and cut out the possibility of missed, lapsed, or repeatedly mortgaged shipments.

- Wealth Management: HSBC and UOB are working with Marketnode to enable native digital issuance of wealth management products, enhancing issuance efficiency and accessibility for investors.

In a testament to the pace of development of the sector, as we wrote this, SIX Digital Exchange announced that UBS issued its first digital bond on the platform, which traded and settled on a regulated exchange by a traditional bank and will also list on the SIX Swiss Exchange. The Tel Aviv, Nasdaq, Australian and London Stock Exchange are other entities that are exploring digital platforms.

Until next week!

The Bequant Team

Martha Reyes

Emiliano Bruno

This document contains information that is confidential and proprietary to Bequant Holding Limited and its affiliates and subsidiaries (the “BEQUANT Group”) and is provided in confidence to the named recipients. The information provided does not constitute investment advice, financial advice, trading advice or any other sort of advice. None of the information on this document constitutes or should be relied on as, a suggestion, offer, or other solicitation to engage in or refrain from engaging in, any purchase, sale, or any other investment-related activity with respect to any transaction. Cryptocurrency investments are volatile and high-risk in nature. Trading cryptocurrencies carries a high level of risk, and may not be suitable for all investors. No part of it may be used, circulated, quoted, or reproduced for distribution beyond the intended recipients and the agencies they represent. If you are not the intended recipient of this document, you are hereby notified that the use, circulation, quoting, or reproducing of this document is strictly prohibited and may be unlawful. This document is being made available for information purposes and shall not form the basis of any contract with the BEQUANT Group.

Any transaction is subject to a contract and a contract will not exist until formal documentation has been signed and considered passed. Whilst the BEQUANT Group has taken all reasonable care to ensure that all statements of fact or opinions contained herein are true and accurate in all material respects, the BEQUANT Group